Redefining Clean Energy Economics

The bond between solar energy and storage is undergoing a profound transformation. What started as a supplemental technology to reduce renewable energy intermittency is now becoming a defining prerequisite to how solar projects are financed, built, and valued. Over half of the utility-scale solar projects coming online in 2026 will be paired with storage.1Policy headwinds, evolving tax incentives, and changing grid conditions are reshaping the market, and the clean energy industry is moving with it. Fully integrated solar-plus-storage systems capable of delivering firm, dispatchable clean power marks a critical turning point in how developers, offtakers, and policymakers think about energy generation and reliability.

Several macro trends are accelerating this evolution. The recent tightening of federal tax credit rules in the U.S. has introduced new requirements for developers urgently looking to safe harbor their projects and optimize project economics and timelines. With the accelerated phaseouts of tax credits for solar and wind and the uncertainty around import tariffs, developers and buyers are looking for ways to safeguard returns and secure long-term stability.

Largely spared by the One Big Beautiful Bill Act (OBBBA) by retaining the longer runway for its tax credit, battery storage allows solar projects to capture higher market value during peak demand periods, while mitigating risks associated with curtailment and negative pricing events — issues that have become highly prevalent in ERCOT and CAISO as renewable energy penetration continues to grow. Storage also provides new sources of revenue for developers including capacity revenue, energy arbitrage, and demand response, when applicable.

From a corporate procurement standpoint, the business case for pairing solar and storage is also strengthening. As Virtual Power Purchase Agreements (VPPA) markets mature, buyers are seeking greater control over the timing and predictability of power generation. Co-located storage lays a pathway to balance exposure to price volatility and align energy production with operational demand profiles. This is particularly relevant as more companies prepare for updates to the GHG Protocol’s Scope 2 guidance, which may require closer matching between energy use and generation on an hourly basis within the same regional market as the company’s energy consumption.

AI and data center buildout remain the leading source of electricity demand growth in North America. A recent forecast suggests that power demand from U.S. data centers is expected to surge to 106 GW by 2035 – a 36 percent jump from a previous outlook published just seven months earlier2. And yet, this is still a conservative projection compared to other industry forecasts. It is expected that some of this demand will be met by natural gas-fired generation. That said, hyperscalers with sustainability goals are driving unprecedented demand for clean firm energy, and solar + storage provides the most cost-effective mechanism to deploy, and the easiest bridge to 24/7 clean power, until other clean baseload options become financially and technologically viable.

Another promising use case of storage is potentially a speedier utility interconnection. This process has been cumbersome, expensive, and frustrating for all parties involved, including data centers and other large loads. By committing to reducing consumption via co-located storage or other distributed resources when the grid is stressed or supply is constrained, large loads could potentially interconnect to the grid faster while avoiding hefty grid infrastructure updates. This would then reduce project development timelines and potential transmission costs.

Lithium-ion batteries remain dominant due to their deployment speed, modularity, and affordability, making them ideal for short-duration needs and peak shaving. However, additional long-duration technologies are rapidly emerging. Over time, these systems will become more commercially viable and can enhance the ability of solar portfolios to participate in ancillary services and capacity markets, creating new layers of energy value.

Contract structures are also evolving to reflect the integration of storage, with developers and offtakers experimenting with two primary models. In one approach, solar generation and battery storage are contracted separately, often through a traditional PPA for the renewable asset and a tolling or capacity agreement for the battery. This structure provides flexibility for financiers and operators to manage risk independently.

Alternatively, fully integrated hybrid PPAs, however more complex, combine multiple assets like solar, wind, and battery storage under a single agreement, allowing the buyer to procure optimized energy delivery while the project operator leverages storage for price arbitrage and grid services. Hybrid PPAs assist in times of high intermittency or market volatility, providing greater consistency of power generation and deployment. Each approach carries unique commercial implications, but both reflect a broader industry move towards flexibility and dispatchable clean energy solutions.

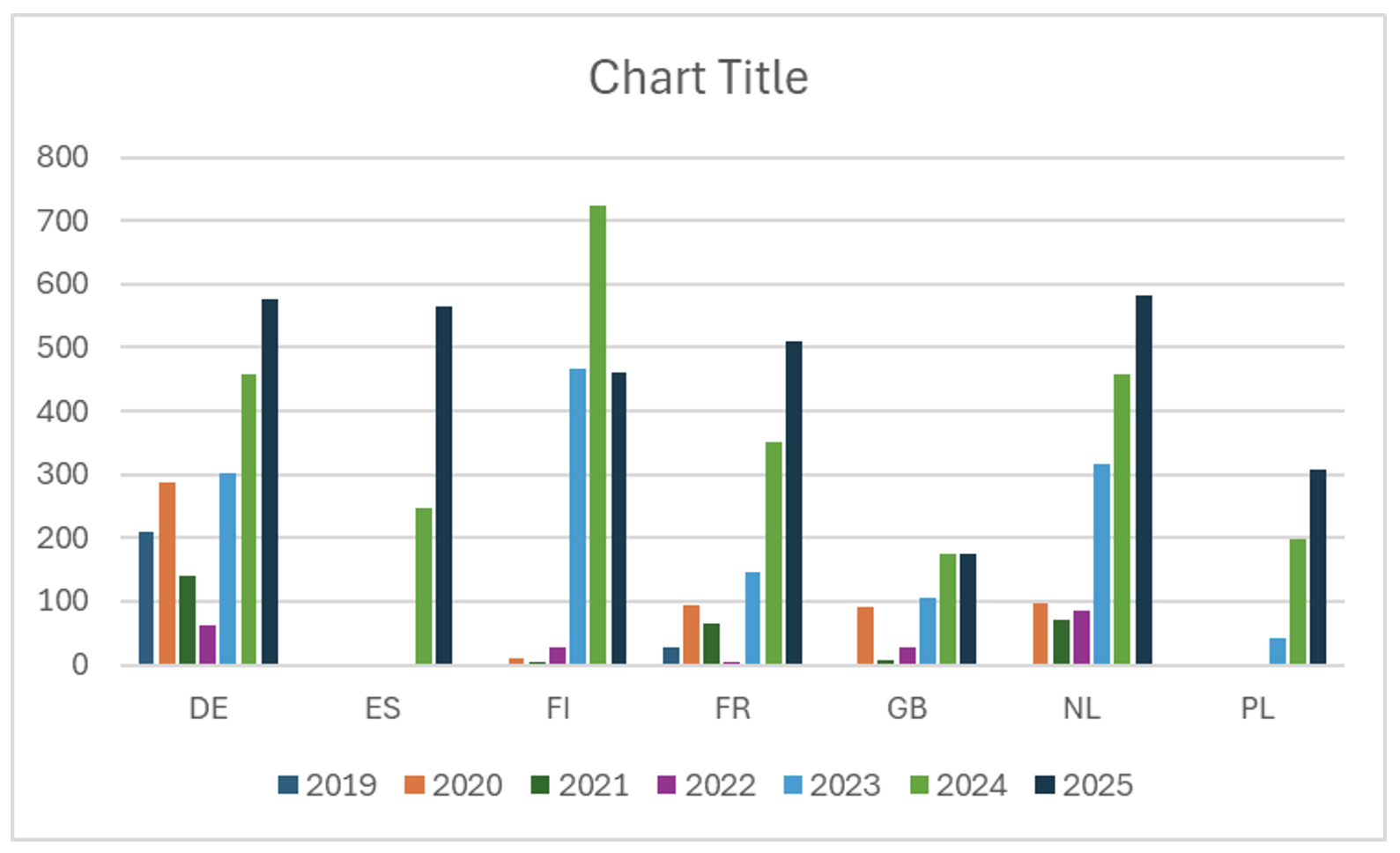

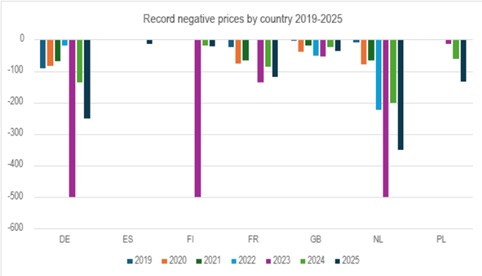

This trend is visible not only in North America but also across Europe, where developers are increasingly bundling storage with solar to mitigate negative price exposure. In 2025, Europe experienced an increase in the number of negative price hours across most European electricity markets. For example, the Netherlands reported 507 instances of negative electricity prices, exceeding the 458 occurrences seen throughout 2024, according to reports.3 In countries such as Germany, Spain, and the UK, hybrid projects now represent a growing share of PPA opportunities. These projects are strategically designed to reduce curtailment, stabilize revenue streams, and enhance the overall reliability of renewable portfolios — a model that North American developers are beginning to emulate as market dynamics converge.

Negative price events in EU 2019-2025. Source: ENTSO-E

Record negative prices by country 2019-2025. Source: ENTSO-E

Looking ahead, as energy demand from data centers, electrification, and reshoring continues to rise, flexible and dispatchable energy solutions will be essential to maintaining reliability and affordability. The next phase of market development will likely focus on value stacking, integrating revenue from energy arbitrage, capacity payments, and ancillary services alongside long-duration storage technologies that can extend renewable generation through the evening hours.

The relationship between solar and storage is no longer one of dependency but of cohesion. Together, they are reshaping the economics, reliability, and perception of renewable energy. For utilities, corporates, and investors alike, understanding this evolving synergy is key to capturing value in a market where flexibility has become the new foundation of competitiveness.

Hannah Badrei is Senior Vice President, Global Energy Advisory Services, and Joey Lange is Senior Managing Director, Sustainability & Clean Energy at Trio, a global energy and sustainability advisory company that helps organizations navigate the energy transition.

Trio | www.trioadvisory.com

References

- Keith Adams et al., “2026 Renewable Energy Industry Outlook,” Deloitte, October 29, 2025

- AI and the Power Grid: Where the Rubber Meets the Road | BloombergNEF

- “Global Renewables Market Report: Second Half 2025,” Trio, October 20, 2025

Author: Hannah Badrei, Ph.D. and Joey Lange