.jpg?r=1143)

As technological advancements occur through new developments in the offshore wind energy industry, there will be times where these large projects may impact the cultural heritage of humanity's past in our waters. Federal, State, and Tribal government agencies in the United States have regulations in place to protect archaeological cultural resources within and outside their territorial boundaries. The success of offshore projects relies on buildi....

The growth and rapid evolution of the offshore wind industry and the introduction of new, US Jones Act-compliant offshore wind vessels mean that wind operations may involve the use of Jones Act seamen, maritime employees, and other non-maritime employees. Such workers variously fall under the purview of the Jones Act, the Longshore and Harbor Workers’ Compensation Act (LHWCA), and other laws that determine their rights and remedies in cases of ....

The allure of wind turbines is undeniable. For those fortunate enough to visit these engineering marvels, it’s an experience filled with awe and learning. However, the magnificence of these structures comes with inherent risks, making safety an absolute priority. The prior safety training of participants in courses like ‘Limited Access’ (a standardized course approved by The Global Wind Organization) plays a crucial role in ensuring visitor....

Identifying trees, grasslands, and wetlands on landscape-scale project sites has never been simple or clear-cut. Aerial photos are subject to divergent interpretations. Field surveys incur higher costs from hours spent documenting and mapping observations, and datasets such as the National Land Cover Database can be too coarse to capture nuances in the terrain. While landscapes change constantly, regulatory officials request informati....

Sion Power Corporation, a leading technology developer of next-generation batteries for electric vehicles (EV), and MB ATECH, member of Muhlbauer Group, a German turnkey solution provider, announced a partnership to create an automated manufacturing line for Sion Power’s large format lithium metal cell.

The new fully-automated manufacturing line will be capable of producing 75MWh of 56 Ah lithium metal cells annually. Sion Power's strategic partnership with Muhlbauer is an instrumental next step in our path to commercialization. It increases cell production capabilities with a fully automated manufacturing line. These cells will be provided to automotive OEMs, cell manufacturers and others to fully test Sion Power’s Licerion technology, which will offer reduced range anxiety by substantially increasing the driving range or better utilization of energy per unit weight when compared to conventional lithium-ion cells.

“We are pleased to collaborate with Muhlbauer’s team to deploy our 56Ah cell after years of research and development. Through this collaboration, we are able to take another strong step in demonstrating the scalability of Licerion. We are confident in our ability to deliver reliable and robust cells to our partners. This line will help bolster the domestic supply chain of lithium metal cells and position Sion Power as an industry leader in the industrialization of energy storage systems,” said Tracy Kelley, Sion Power’s CEO.

"Mühlbauer is looking forward to a strong partnership with Sion Power as a great player in the battery industry. Leveraging Sion Power’s expertise in the future battery technology and Mühlbauer’s technical expertise in special machine and serial production, this partnership will be a successful one. The rapid growth of the battery industry enables advancements to next-generation technologies in notching, stacking and cell assembly," said Josef Markus Mühlbauer, General Manager of MB ATECH, the eMobility division of the Mühlbauer Group.

Sion Power | sionpower.com

Mühlbauer Group | www.muhlbauer.com

LF Energy, the open source foundation focused on harnessing the power of collaborative software and hardware technologies to accelerate the energy transition, is pleased to announce that four new open source technical projects and three new working groups have been accepted into the foundation. These initiatives will provide the energy sector with new resources around digital substations, preparing for extreme weather events, taking advantage of advances in data and AI technologies, and more. This comes ahead of the Open Sustainability Policy Summit and Open EV Charging Summit, both of which LF Energy is hosting with partners in May.

Four New Open Source Projects

The LF Energy Technical Advisory Council has voted to accept four new projects into the foundation. Two of these projects are focused on making better use of open data to address challenges in the energy transition, while the other two will help with modeling for extreme weather events, and digital substations. The addition of these projects further strengthens LF Energy's overall tech stack, and provides additional open source resources for energy stakeholders looking to transition to renewables. The new projects are:

Three New Working Groups

LF Energy hosts working groups, which bring together communities of disparate stakeholders to identify challenges and develop open source solutions for the energy transition. Working groups may result in the creation of new technical projects, standards, documentation, best practices, or other deliverables to benefit the industry. The three new working groups are:

Upcoming Events

LF Energy is organizing three upcoming events to gather various groups of energy stakeholders to learn and share best practices and open source solutions for the energy transition. These events include:

Members of the media who wish to request media passes for any of these events can contact [email protected].

Additionally, LF Energy Executive Director Alex Thornton will present a session at the upcoming IEEE PES T&D Conference on May 8 in Anaheim, CA, titled "Accelerating grid modernization with open technology and standards".

LF Energy Releases First Annual Report

For the first time, LF Energy has released an annual report, providing detailed insight into the progress made in 2023 in pursuit of its mission to create a technology ecosystem that enables decarbonization of the energy sector through innovation and interoperability. 2023 saw tremendous growth for LF Energy, with nine new projects added to bring the total to 30. Nine new members also joined, contributor strength grew by 30%, and lines of code hosted grew by 22%. The EVerest and SEAPATH projects graduated to the Early Adoption phase, in addition to hosted projects across the board seeing rapid growth in deployments.

Download the full report to learn more.

LF Energy Partners with CRESYM to Enhance Digitalization of Energy Systems Through Open Source

LF Energy has joined forces with CRESYM to accelerate and support the development of open source technologies to enhance the digitalization of energy systems. CRESYM is a non-profit association, gathering industrial and academic research organizations and aiming at solving the coming challenges for the future, fast-evolving European energy system.

The partnership will build on the strengths of both organizations. CRESYM will continue to focus on the creation of new, innovative research projects to drive digital transformation in the energy sector. LF Energy's expertise lies in its knowledge and expertise in building sustainable open source projects and communities to support them. LF Energy is now the preferred organization for hosting CRESYM's research projects when they reach an appropriate stage to enhance their technology readiness levels further and develop them as open source tools.

OwnTech Joins LF Energy

LF Energy recently welcomed OwnTech, a non-profit organization that changes the user experience in power electronics through an open source technology suite, as an Associate Member.

"We are pleased to see support for open source software, hardware, and standards growing to drive the energy transition forward," said LF Energy Executive Director Alex Thornton. "It is essential that all stakeholders work together collaboratively to advance these solutions so the energy sector can digitalize and decarbonize. I encourage anyone interested to get involved, whether that is by contributing new projects or code to existing projects, joining us as a member, or attending one of our upcoming events."

LF Energy Resources

LF Energy | https://www.lfenergy.org

MCE has partnered with Renewable America to bring online another 1 megawatt of solar in Marin County. The 4.5 acre Fallon Two Rock solar farm is MCE's latest local project, generating an estimated 2,300 megawatt hours annually and:

")

To celebrate this milestone, MCE and Renewable America (RNA) hosted a ribbon-cutting ceremony at the site in Petaluma on Monday, April 15.

"We're thrilled to celebrate Fallon's commercial operation and toast the partnership with MCE at the ribbon-cutting," said Ardeshir Arian, President & CEO of RNA. "Renewable America's motto 'Think Local. Act Local,' drives us to prioritize local projects like Fallon Two Rock that positively impact local communities. This is our first project with MCE, supporting local clean energy generation and committing to fast-tracking progress toward a clean energy future in California."

The Fallon Two Rock project came online in January 2024 as part of MCE's 48 megawatts of local energy generation. The project, financed by Sunwest Bank, represents MCE and RNA's commitment to advancing clean energy solutions and fostering sustainable development in the region.

RNA Services LLC, a subsidiary of Renewable America, served as the engineering, procurement, and construction partner and will continue its role in operations and maintenance.

The project is also approved for agricultural compatible land use, allowing continued agricultural operations while generating carbon-free electricity. The employment of several local companies for the project's construction, including Sunstall Inc. and Sierra Tree Company, further demonstrates MCE and RNA's commitment to local development.

Fallon Two Rock was built with nearly 4,000 hours of prevailing wage labor. RNA has also committed $20,000 to MCE for local workforce development.

"Clean energy is just one part of the transition to a sustainable future," said Katie Rice, MCE Board Director and County of Marin Supervisor. "The additional funding RNA committed will help MCE grow the clean energy economy, providing training opportunities for local residents to enter the green workforce."

Fallon Two Rock is MCE's sixteenth Feed-In Tariff (FIT) project to come online in the Bay Area. The FIT program incentivizes local renewable energy development and job creation by paying above market rate for renewable energy generation in MCE's service area. The project is a testament to the collaborative efforts of MCE and RNA in advancing renewable energy and supporting the local economy. View MCE's full list of local projects at mcecleanenergy.org/local-projects.

MCE | mcecleanenergy.org

Renewable America | https://renewam.com

SolaREIT, a solar and storage real estate investment company, has closed $13 million in real estate financings for NineDot Energy's battery energy storage (BESS) projects. NineDot Energy, the leading developer of community-scale BESS in the New York City metropolitan area, has a significant pipeline of projects throughout New York City, Westchester County and Long Island. The deal is SolaREIT's first stand-alone battery storage deal completed after the company announced the expansion of their clean energy real estate financing solutions to storage developers. SolaREIT, founded in 2020, offers land purchase, lease purchase and renewable land loans to clean energy developers in both the storage and solar industries.

"Battery storage is foundational to downstate New York's energy transition – but to build out these sites, developers require significant capital from a variety of financial partners, " said David Arfin, CEO and co-founder of NineDot Energy. "SolarREIT understood our business needs and tailored a product that supported our purchase of some sites for our battery storage projects."

"We are delighted to work with NineDot Energy to support the development of community-scale BESS projects in the New York City metro area. Expansion of battery energy storage in urban areas is critical to stabilizing the grid and bringing more renewables online. We are able to empower developers with the capital and financial flexibility they need, allowing them to focus on their core expertise: creating impactful clean energy projects," said Laura Pagliarulo, President of SolaREIT.

SolaREIT | https://www.solareit.com

NineDot Energy | nine.energy

Ballard Power Systems (NASDAQ: BLDP) (TSX: BLDP) announced multiple purchase orders totaling 70 FCmove-HD hydrogen fuel cell engines from its customer Wrightbus, a UK-based bus manufacturer deploying hydrogen-powered buses in the UK and Europe. Ballard expects delivery of the fuel cell engines to occur in 2024, and the buses to enter into service in 2025. The hydrogen fuel cell engines will power single- and double-decker buses in the UK and Germany.

"We are pleased to strengthen our relationship with Wrightbus and support their deployment of an increasing volume of hydrogen-powered transit buses across the UK and Europe," said Oben Uluc, Vice President, Sales & Marketing, EMEA. "We are seeing broader market acceptance of fuel cell buses by European transit operators seeking to decarbonize their operations with a technology approach that enables long range, fast refueling, and scalable refueling infrastructure."

Ballard Power Systems | www.ballard.com

Wrightbus | https://wrightbus.com/

Nova Clean Energy (‘Nova’) announced the acquisition of HyFuels, a more than 1 gigawatt portfolio of mid-to-late-stage wind and solar development projects as well as an earlier stage green ammonia project. Located on the Texas Gulf Coast, an area of rapidly increasing power demand and a leading center for American-produced ammonia, HyFuels is ideally situated to serve the petrochemical industry, ensuring Texas remains the global leader in this essential industry.

HyFuels, which has a current project footprint of about 25,000 acres, has a power supply that is split evenly between wind and solar, whose complementary generation profiles will ensure a steady supply of clean local power. The first phase of the project is expected to reach Full Notice to Proceed (NTP) in 2025 and Commercial Operations in 2026.

Nova acquired HyFuels from BNB Renewable Energy (‘BNB’), a developer with a nearly 20-year track record of developing wind and solar projects across the United States and in Mexico, including for a range of industrial clients. Nova has entered into a long-term development services agreement with BNB, which originated the development in late 2020, ensuring full alignment on the successful delivery of the HyFuels project.

Since initially partnering in mid-2023, Nova and BNB have worked to advance the HyFuels complex, including completing necessary environmental surveys, securing a workable schedule for connection to the power grid, and ordering long lead-time equipment.

Commenting on the announcement, Ben Pratt, President of Nova Clean Energy, said, “The Texas grid is going to continue to need a variety of power sources to serve its fast-growing demand. Wind paired with solar provides a generation profile that industrial as well as utility customers increasingly want to see. We are excited to work with BNB on this important portfolio.”

Commenting on the announcement, Jos Nicholas, CEO of BNB, said, “This is an exciting project, and we’re pleased to have partnered with the Nova Clean Energy team to bring it to market. A lot of important stakeholders have come together to help us get to this point, and we want to thank the landowners, community members and local officials, including the county commissioners, the ISD, and the VEDC, for their ongoing support. Together, we and Nova look forward to working with and learning from this community in Calhoun and Victoria counties in order to bring low-cost electricity and green ammonia to this amazingly productive part of Texas and our nation’s economy.”

Since its formation in 2022, Nova has grown rapidly across wind, solar and battery storage. Nova’s project pipeline is positioned to benefit from 3 core themes: expansion and strengthening of transmission networks, new end-customer demand in areas like mobility, green fuels and AI, as well as growing build-transfer opportunities driven by increased utility ownership. With a project pipeline that now exceeds 5 GW of projects in 8 states and multiple power markets (including WECC, MISO & ERCOT), and with marked acceleration in each of its core development themes, Nova is positioned for rapid future growth.

Nova Clean Energy | https://www.novacleanenergyllc.com/

Bluestar Energy Capital | https://www.bluestarenergycapital.com/

BNB Renewable Energy | www.bnbrenewables.com

Next week, the global offshore wind industry will convene in New Orleans for the International Partnering Forum (IPF), the largest offshore wind conference in the Americas. Hosted by Oceantic Network April 22-25 at the Ernest N. Morial Convention Center, IPF will convene key decision makers, stakeholders, and companies to discuss the future of offshore wind in the U.S. as it begins construction on several new commercial-scale projects, tackles the adoption of floating offshore wind on both the East and West Coasts, and identifies the challenges and opportunities in building out a robust domestic supply chain.

IPF Week will kick off Monday, April 22, with a series of all-day tours highlighting Louisiana’s offshore, port, and manufacturing infrastructure highlighting how the region will support the growing offshore wind industry. Also on Monday is a U.S. Offshore Wind Market Update, giving attendees a detailed overview of the market and featuring a series of speakers and panels providing the latest critical news and regional insights.

On Tuesday, IPF will host the U.S. Offshore Wind Workforce Summit, a gathering of workforce development leaders, industry experts, government officials, and others to create solutions to address offshore wind industry workforce needs. in partnership with the National Renewable Energy Laboratory (NREL). Oceantic Network will also host the U.S. Offshore Wind Standards Initiative, gathering industry to discuss ideas for greater standardization within the offshore wind supply chain. Later in the day, the exhibit hall opens, kicking off with What’s New & Spinning, a series of interviews with the industry’s top developers, as well as the series of workshops and Networking receptions. The day will conclude with the U.S. premiere of the documentary Planet Wind at the Civic Theater.

IPF’s Plenary Session will take place on Wednesday, April 24. IPF attendees will hear remarks from U.S. Secretary of the Interior Deb Haaland, Deputy Secretary of Energy David Turk, Best-selling author Dan Gardner, NYSERDA President and CEO Doreen Harris, Oceantic Network CEO Liz Burdock, and more (full list below).

“This year’s IPF is bringing more content than ever to support the offshore wind industry,” said Liz Burdock, founder and CEO of Oceantic Network. “In addition, we’ve expanded our programming to place a greater focus on floating offshore wind and highlight the introduction of floating solar, tidal, and other ocean renewable energies. IPF is the place to be for all businesses working in offshore wind; whether you’re just starting out or have years of experience, there’s an abundance of knowledge and insight to be gained at IPF.”

For the first time, IPF will host a two-day FloatON Summit beginning Wednesday, April 24. The first-ever Summit will focus on knowledge sharing, best practices, and innovations required for the U.S. to implement floating offshore wind along the East and West Coasts. The FloatON Summit will draw on the expertise of IPF attendees and convene the best and brightest minds to explain the market conditions, policy enablers, and financial and insurance mechanisms necessary to make floating offshore wind technology competitive and realize commercialization in the United States.

This year’s IPF is on track to welcome thousands of industry professionals from around the globe, all focused on sharing valuable insights and making connections to move the emerging U.S. wind industry forward. Attendees will have access to nearly 400 exhibitors in the Exhibit Hall, more than 350 experts speaking on the latest developments, projects, and products moving the offshore wind industry and its supply chain forward, and a range of networking opportunities, including WindMatch™ one-on-one appointments and Tuesday’s IPF Opening Reception.

IPF Week Highlights: April 22-25

Presented by the Oceantic Network

Ernest N. Morial Convention Center

900 Convention Center Boulevard

New Orleans, LA 70130

Access the full schedule online.

For press credentials, register online here. Live video coverage will be available for the Plenary Session only, contact us for more details.

Host sponsors for 2024 IPF are bp, Fugro, RWE, and Shell.

April 22

Local Offshore Wind Industry Tours

All Day

Bayou Lafourche Port and Offshore Training Tour

Morgan City’s Offshore Expertise Tour – From Ports to Shipbuilding

Beach to Blade Tour: Offshore Wind Research and Innovation

U.S. Offshore Wind Market Update: Benefits of Regional Supply Chain Collaboration

1 p.m. to 5 p.m.

This session will be a comprehensive introduction to the U.S. market. Panelists will provide a broad summary of the sector, discussing both hurdles and opportunities. Additionally, officials from multiple federal government agencies and nearly 10 U.S. states will present insights on their unique initiatives. The day will close with a panel featuring members of the Network’s new West Coast Supplier Council.

April 23

U.S. Offshore Wind Workforce Summit

9 a.m. to 4 p.m.

U.S. Offshore Wind Standards Initiative

9 a.m. to 4 p.m.

Exhibit Hall Opens

1 p.m.

April 24

Plenary Session

8:30 a.m. – 10:30 a.m.

Liz Burdock, President & CEO, Oceantic Network

Dan Gardner, Best-Selling Author, “How Big Things Get Done”

Doreen Harris, President and CEO, NYSERDA

U.S. Deputy Secretary of Energy David Turk

Amanda Dasch, Vice President of Renewable Generation Americas – Shell Energy Americas

Panel – The Next Chapter: Taking U.S. Offshore Wind from Planning to Construction

Céline B. Gerson, President and Group Director Americas, Fugro; Ryan Donnelly, Commercial Director, Atlantic Shores; Joshua Weinstein, President, Offshore Wind Americas, bp; Amanda Lefton, Vice President of Development, U.S. East, RWE; moderated by Bloomberg Reporter Josh Saul

U.S. Secretary of the Interior Deb Haaland

FloatON Summit

2 p.m. to 5 p.m.

Maine Governor Janet Mills

April 25

Regional Breakfast Briefings

8:30 a.m. to 9:30 a.m.

FloatON Summit: Day 2

9:45 a.m. to 4:30 p.m.

Oceantic Network | https://oceantic.org/

Alternative Energies May 15, 2023

The United States is slow to anger, but relentlessly seeks victory once it enters a struggle, throwing all its resources into the conflict. “When we go to war, we should have a purpose that our people understand and support,” as former Secretary ....

Unleashing trillions of dollars for a resilient energy future is within our grasp — if we can successfully navigate investment risk and project uncertainties.

The money is there — so where are the projects?

A cleaner and more secure energy future will depend on tapping trillions of dollars of capital. The need to mobilize money and markets to enable the energy transition was one of the key findings of one of the largest studies ever conducted among the global energy sector C-suite. This will mean finding ways to reduce the barriers and uncertainties that prevent money from flowing into the projects and technologies that will transform the energy system. It will also mean fostering greater collaboration and alignment among key players in the energy space.

Interestingly, the study found that insufficient access to finance was not considered the primary cause of the current global energy crisis. In fact, capital was seen to be available — but not being unlocked. Why is that? The answer lies in the differing risk profiles of energy transition investments around the world. These risks manifest in multiple ways, including uncertainties relating to project planning, public education, stakeholder engagement, permitting, approvals, policy at national and local levels, funding and incentives, technology availability, and supply chains.

Interestingly, the study found that insufficient access to finance was not considered the primary cause of the current global energy crisis. In fact, capital was seen to be available — but not being unlocked. Why is that? The answer lies in the differing risk profiles of energy transition investments around the world. These risks manifest in multiple ways, including uncertainties relating to project planning, public education, stakeholder engagement, permitting, approvals, policy at national and local levels, funding and incentives, technology availability, and supply chains.

These risks need to be addressed to create more appealing investment opportunities for both public and private sector funders. This will require smart policy and regulatory frameworks that drive returns from long-term investment into energy infrastructure. It will also require investors to recognize that resilient energy infrastructure is more than an ESG play — it is a smart investment in the context of doing business in the 21st century.

Make de-risking investment profiles a number one priority

According to the study, 80 percent of respondents believe the lack of capital being deployed to accelerate the transition is the primary barrier to building the infrastructure required to improve energy security. At the same time, investors are looking for opportunities to invest in infrastructure that meets ESG and sustainability criteria. This suggests an imbalance between the supply and demand of capital for energy transition projects.

How can we close the gap?

One way is to link investors directly to energy companies. Not only would this enable true collaboration and non-traditional partnerships, but it would change the way project financing is conceived and structured — ultimately aiding in potentially satisfying the risk appetite of latent but hugely influential investors, such as pension funds. The current mismatch of investor appetite and investable projects reveals a need for improving risk profiles, as well as a mindset shift towards how we bring investment and developer stakeholders together for mutual benefit. The circular dilemma remains: one sector is looking for capital to undertake projects within their skill to deploy, while another sector wonders where the investable projects are.

This conflict is being played out around the world; promising project announcements are made, only to be followed by slow progress (or no action at all). This inertia results when risks are compounded and poorly understood. To encourage collaboration between project developers and investors with an ESG focus, more attractive investment opportunities can be created by pulling several levers: public and private investment strategies, green bonds and other sustainable finance instruments, and innovative financing models such as impact investing.

Expedite permitting to speed the adoption of new technologies

Another effective strategy to de-risk investment profiles is found in leveraging new technologies and approaches that reduce costs, increase efficiency, and enhance the reliability of energy supply. Research shows that 62 percent of respondents indicated a moderate or significant increase in investment in new and transitional technologies respectively, highlighting the growing interest in innovative solutions to drive the energy transition forward.

Hydrogen, carbon capture and storage, large-scale energy storage, and smart grids are some of the emerging technologies identified by survey respondents as having the greatest potential to transform the energy system and create new investment opportunities. However, these technologies face challenges such as long lag times between conception and implementation.

If the regulatory environment makes sense, then policy uncertainty is reduced, and the all-important permitting pathways are well understood and can be navigated. Currently, the lack of clear, timely, and fit-for-purpose permitting is a major roadblock to the energy transition. To truly unleash the potential of transitional technologies requires the acceleration of regulatory systems that better respond to the nuance and complexity of such technologies (rather than the current one-size-fits all approach). In addition, permitting processes must also be expedited to dramatically decrease the period between innovation, commercialization, and implementation. One of the key elements of faster permitting is effective consultation with stakeholders and engagement with communities where these projects will be housed for decades. This is a highly complex area that requires both technical and communication skills.

The power of collaboration, consistency, and systems thinking

The report also reveals the need for greater collaboration among companies in the energy space to build a more resilient system. The report shows that, in achieving net zero, there is a near-equal split between those increasing investment (47 percent of respondents), and those decreasing investment (39 percent of respondents). This illustrates the complexity and diversity of the system around the world. A more resilient system will require all its components – goals and actions – to be aligned towards a common outcome.

Another way to de-risk the energy transition is to establish consistent, transparent, and supportive policy frameworks that encourage investment and drive technological innovation. The energy transition depends on policy to guide its direction and speed by affecting how investors feel and how the markets behave. However, inconsistent or inadequate policy can also be a source of uncertainty and instability. For example, shifting political priorities, conflicting international standards, and the lack of market-based mechanisms can hinder the deployment of sustainable technologies, resulting in a reluctance to commit resources to long-term projects.

Variations in country-to-country deployment creates disparities in energy transition progress. For instance, the 2022 Inflation Reduction Act in the US has posed challenges for the rest of the world, by potentially channeling energy transition investment away from other markets and into the US. This highlights the need for a globally unified approach to energy policy that balances various national interests while addressing a global problem.

To facilitate the energy transition, it is imperative to establish stable, cohesive, and forward-looking policies that align with global goals and standards. By harmonizing international standards, and providing clear and consistent signals, governments and policymakers can generate investor confidence, helping to foster a robust energy ecosystem that propels the sector forward.

Furthermore, substantive and far-reaching discussions at international events like the United Nations Conference of the Parties (COP), are essential to facilitate this global alignment. These events provide an opportunity to de-risk the energy transition through consistent policy that enables countries to work together, ensuring that the global community can tackle the challenges and opportunities of the energy transition as a united front.

Keeping net-zero ambitions on track

Despite the challenges faced by the energy sector, the latest research reveals a key positive: 91 percent of energy leaders surveyed are working towards achieving net zero. This demonstrates a strong commitment to the transition and clear recognition of its importance. It also emphasizes the need to accelerate our efforts, streamline processes, and reduce barriers to realizing net-zero ambitions — and further underscores the need to de-risk energy transition investment by removing uncertainties.

The solution is collaborating and harmonizing our goals with the main players in the energy sector across the private and public sectors, while establishing consistent, transparent, and supportive policy frameworks that encourage investment and drive technological innovation.

These tasks, while daunting, are achievable. They require vision, leadership, and action from all stakeholders involved. By adopting a new mindset about how we participate in the energy system and what our obligations are, we can stimulate the rapid progress needed on the road to net zero.

Dr. Tej Gidda (Ph.D., M.Sc., BSc Eng) is an educator and engineer with over 20 years of experience in the energy and environmental fields. As GHD Global Leader – Future Energy, Tej is passionate about moving society along the path towards a future of secure, reliable, and affordable low-carbon energy. His focus is on helping public and private sector clients set and deliver on decarbonization goals in order to achieve long-lasting positive change for customers, communities, and the climate. Tej enjoys fostering the next generation of clean energy champions as an Adjunct Professor at the University of Waterloo Department of Civil and Environmental Engineering.

GHD | www.ghd.com

The Kincardine floating wind farm, located off the east coast of Scotland, was a landmark development: the first commercial-scale project of its kind in the UK sector. Therefore, it has been closely watched by the industry throughout its installation. With two of the turbines now having gone through heavy maintenance, it has also provided valuable lessons into the O&M processes of floating wind projects.

In late May, the second floating wind turbine from the five-turbine development arrived in the port of Massvlakte, Rotterdam, for maintenance. An Anchor Handling Tug Supply (AHTS)

vessel was used to deliver the KIN-02 turbine two weeks after a Platform Supply Vessel (PSV) and AHTS had worked to disconnect the turbine from the wind farm site. The towing vessel became the third vessel used in the operation.

This is not the first turbine disconnected from the site and towed for maintenance. In the summer of 2022, KIN-03 became the world’s first-ever floating wind turbine that required heavy maintenance (i.e. being disconnected and towed for repair). It was also towed from Scotland to Massvlakte.

Each of these operations has provided valuable lessons for the ever-watchful industry in how to navigate the complexities of heavy maintenance in floating wind as the market segment grows.

The heavy maintenance process

When one of Kincardine’s five floating 9.5 MW turbines (KIN-03) suffered a technical failure in May 2022, a major technical component needed to be replaced. The heavy maintenance strategy selected by the developer and the offshore contractors consisted in disconnecting and towing the turbine and its floater to Rotterdam for maintenance, followed by a return tow and re-connection. All of the infrastructure, such as crane and tower access, remained at the quay following the construction phase. (Note, the following analysis only covers KIN-03, as details of the second turbine operation are not yet available).

Comparing the net vessel days for both the maintenance and the installation campaigns at this project highlights how using a dedicated marine spread can positively impact operations.

For this first-ever operation, a total of 17.2 net vessel days were required during turbine reconnection—only a slight increase on the 14.6 net vessel days that were required for the first hook-up operation performed during the initial installation in 2021. However, it exceeds the average of eight net vessel days during installation. The marine spread used in the heavy maintenance operation differed from that used during installation. Due to this, it did not benefit from the learning curve and experience gained throughout the initial installation, which ultimately led to the lower average vessel days.

The array cable re-connection operation encountered a similar effect. The process was performed by one AHTS that spent 10 net vessel days on the operation. This compares to the installation campaign, where the array cable second-end pull-in lasted a maximum of 23.7 hours using a cable layer.

Overall, the turbine shutdown duration can be broken up as 14 days at the quay for maintenance, 52 days from turbine disconnection to turbine reconnection, and 94 days from disconnection to the end of post-reconnection activities.

What developers should keep in mind for heavy maintenance operations

This analysis has uncovered two main lessons developers should consider when planning a floating wind project: the need to identify an appropriate O&M port, and to guarantee that a secure fleet is available.

Floating wind O&M operations require a port with both sufficient room and a deep-water quay. The port must also be equipped with a heavy crane with sufficient tip height to accommodate large floaters and reach turbine elevation. Distance to the wind farm should also be taken into account, as shorter distances will reduce towing time and, therefore, minimize transit and non-productive turbine time.

During the heavy maintenance period for KIN-03 and KIN-02, the selected quay (which had also been utilized in the initial installation phase of the wind farm project), was already busy as a marshalling area for other North Sea projects. This complicated the schedule significantly, as the availability of the quay and its facilities had to be navigated alongside these other projects. This highlights the importance of abundant quay availability both for installation (long-term planning) and maintenance that may be needed on short notice.

At the time of the first turbine’s maintenance program (June 2022), the North Sea AHTS market was in an exceptional situation: the largest bollard pull AHTS units contracted at over $200,000 a day, the highest rate in over a decade.

During this time, the spot market was close to selling out due to medium-term commitments, alongside the demand for high bollard pull vessels for the installation phase at a Norwegian floating wind farm project. The Norwegian project required the use of four AHTS above a 200t bollard pull. With spot rates ranging from $63,000 to $210,000 for the vessels contracted for Kincardine’s maintenance, the total cost of the marine spread used in the first repair campaign was more than $4 million.

Developers should therefore consider the need to structure maintenance contracts with AHTS companies, either through frame agreements or long-term charters, to decrease their exposure to spot market day rates as the market tightens in the future.

While these lessons are relevant for floating wind developers now, new players are looking towards alternative heavy O&M maintenance options for the future. Two crane concepts are especially relevant in this instance. The first method is for a crane to be included in the turbine nacelle to be able to directly lift the component which requires repair from the floater, as is currently seen on onshore turbines. This method is already employed in onshore turbines and could be applicable for offshore. The second method is self-elevating cranes with several such solutions already in development.

The heavy maintenance operations conducted on floating turbines at the Kincardine wind farm have provided invaluable insights for industry players, especially developers. The complex process of disconnecting and towing turbines for repairs highlights the need for meticulous planning and exploration of alternative maintenance strategies, some of which are already in the pipeline. As the industry evolves, careful consideration of ports, and securing fleet contracts, will be crucial in driving efficient and cost-effective O&M practices for the floating wind market.

Sarah McLean is Market Research Analyst at Spinergie, a maritime technology company specializing in emission, vessel performance, and operation optimization.

Spinergie | www.spinergie.com

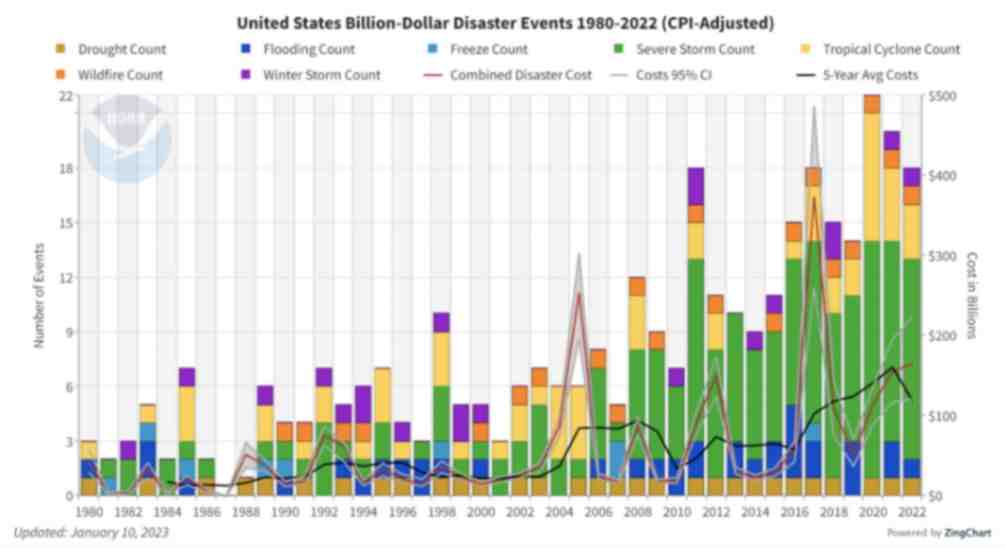

According to the Energy Information Administration (EIA), developers plan to add 54.5 gigawatts (GW) of new utility-scale electric generating capacity to the U.S. power grid in 2023. More than half of this capacity will be solar. Wind power and battery storage are expected to account for roughly 11 percent and 17 percent, respectively.

A large percentage of new installations are being developed in areas that are prone to extreme weather events and natural disasters (e.g., Texas and California), including high wind, tornadoes, hail, flooding, earthquakes, wildfires, etc. With the frequency and severity of many of these events increasing, project developers, asset owners, and tax equity partners are under growing pressure to better understand and mitigate risk.

Figure 1. The history of billion-dollar disasters in the United States each year from 1980 to 2022 (source: NOAA)

In terms of loss prevention, a Catastrophe (CAT) Modeling Study is the first step to understanding the exposure and potential financial loss from natural hazards or extreme weather events. CAT studies form the foundation for wider risk management strategies, and have significant implications for insurance costs and coverage.

Despite their importance, developers often view these studies as little more than a formality required for project financing. As a result, they are often conducted late in the development cycle, typically after a site has been selected. However, a strong case can be made for engaging early with an independent third party to perform a more rigorous site-specific technical assessment. Doing so can provide several advantages over traditional assessments conducted by insurance brokerage affiliates, who may not possess the specialty expertise or technical understanding needed to properly apply models or interpret the results they generate. One notable advantage of early-stage catastrophe studies is to help ensure that the range of insurance costs, which can vary from year to year with market forces, are adequately incorporated into the project financial projections.

The evolving threat of natural disasters

Over the past decade, the financial impact of natural hazard events globally has been almost three trillion dollars. In the U.S. alone, the 10-year average annual cost of natural disaster events exceeding $1 billion increased more than fourfold between the 1980s ($18.4 billion) and the 2010s ($84.5 billion).

Investors, insurers, and financiers of renewable projects have taken notice of this trend, and are subsequently adapting their behavior and standards accordingly. In the solar market, for example, insurance premiums increased roughly four-fold from 2019 to 2021. The impetus for this increase can largely be traced back to a severe storm in Texas in 2019, which resulted in an $80 million loss on 13,000 solar panels that were damaged by hail.

The event awakened the industry to the hazards severe storms present, particularly when it comes to large-scale solar arrays. Since then, the impact of convective weather on existing and planned installations has been more thoroughly evaluated during the underwriting process. However, far less attention has been given to the potential for other natural disasters; events like floods and earthquakes have not yet resulted in large losses and/or claims on renewable projects (including wind farms). The extraordinary and widespread effect of the recent Canadian wildfires may alter this behavior moving forward.

A thorough assessment, starting with a CAT study, is key to quantifying the probability of their occurrence — and estimating potential losses — so that appropriate measures can be taken to mitigate risk.

All models are not created equal

Industrywide, certain misconceptions persist around the use of CAT models to estimate losses from an extreme weather event or natural disaster.

Often, the perception is that risk assessors only need a handful of model inputs to arrive at an accurate figure, with the geographic location being the most important variable. While it’s true that many practitioners running models will pre-specify certain project characteristics regardless of the asset’s design (for example, the use of steel moment frames without trackers for all solar arrays in a given region or state), failure to account for even minor details can lead to loss estimates that are off by multiple orders of magnitude.

The evaluation process has recently become even more complex with the addition of battery energy storage. Relative to standalone solar and wind farms, very little real-world experience and data on the impact of extreme weather events has been accrued on these large-scale storage installations. Such projects require an even greater level of granularity to help ensure that all risks are identified and addressed.

Even when the most advanced modeling software tools are used (which allow for thousands of lines of inputs), there is still a great deal that is subject to interpretation. If the practitioner does not possess the expertise or technical ability needed to understand the model, the margin for error can increase substantially. Ultimately, this can lead to overpaying for insurance. Worse, you may end up with a policy with insufficient coverage. In both cases, the profitability of the asset is impacted.

Supplementing CAT studies

In certain instances, it may be necessary to supplement CAT models with an even more detailed analysis of the individual property, equipment, policies, and procedures. In this way, an unbundled risk assessment can be developed that is tailored to the project. Supplemental information (site-specific wind speed studies and hydrological studies, structural assessment, flood maps, etc.) can be considered to adjust vulnerability models.

This provides an added layer of assurance that goes beyond the pre-defined asset descriptions in the software used by traditional studies or assessments. By leveraging expert elicitations, onsite investigations, and rigorous engineering-based methods, it is possible to discretely evaluate asset-specific components as part of the typical financial loss estimate study: this includes Normal Expected Loss (NEL), also known as Scenario Expected Loss (SEL); Probable Maximum Loss (PML), also known as Scenario Upper Loss (SUL); and Probabilistic Loss (PL).

Understanding the specific vulnerabilities and consequences can afford project stakeholders unique insights into quantifying and prioritizing risks, as well as identifying proper mitigation recommendations.

Every project is unique

The increasing frequency and severity of natural disasters and extreme weather events globally is placing an added burden on the renewable industry, especially when it comes to project risk assessment and mitigation. Insurers have signaled that insurance may no longer be the main basis for transferring risk; traditional risk management, as well as site and technology selection, must be considered by developers, purchasers, and financiers.

As one of the first steps in understanding exposure and the potential capital loss from a given event, CAT studies are becoming an increasingly important piece of the risk management puzzle. Developers should treat them as such by engaging early in the project lifecycle with an independent third-party practitioner with the specialty knowledge, tools, and expertise to properly interpret models and quantify risk.

Hazards and potential losses can vary significantly depending on the project design and the specific location. Every asset should be evaluated rigorously and thoroughly to minimize the margin for error, and maximize profitability over its life.

Chris LeBoeuf is Global Head of the Extreme Loads and Structural Risk division of ABS Group, based in San Antonio, Texas. He leads a team of more than 60 engineers and scientists in the US, UK, and Singapore, specializing in management of risks to structures and equipment related to extreme loading events, including wind, flood, seismic and blast. Chris has more than 20 years of professional experience as an engineering consultant, and is a recognized expert in the study of blast effects and blast analysis, as well as design of buildings. He holds a Bachelor of Science in Civil Engineering from The University of Texas at San Antonio, and is a registered Professional Engineer in 12 states.

Chris LeBoeuf is Global Head of the Extreme Loads and Structural Risk division of ABS Group, based in San Antonio, Texas. He leads a team of more than 60 engineers and scientists in the US, UK, and Singapore, specializing in management of risks to structures and equipment related to extreme loading events, including wind, flood, seismic and blast. Chris has more than 20 years of professional experience as an engineering consultant, and is a recognized expert in the study of blast effects and blast analysis, as well as design of buildings. He holds a Bachelor of Science in Civil Engineering from The University of Texas at San Antonio, and is a registered Professional Engineer in 12 states.

ABS Group | www.abs-group.com

Throughout my life and career as a real estate developer in New York City, I’ve had many successes. In what is clearly one of my most unusual development projects in a long career filled with them, I initiated the building of a solar farm to help t....

I’m just going to say it, BIPV is dumb. Hear me out…. Solar is the most affordable form of energy that has ever existed on the planet, but only because the industry has been working towards it for the past 15 years. Governments,....

Heat waves encircled much of the earth last year, pushing temperatures to their highest in recorded history. The water around Florida was “hot-tub hot” — topping 101° and bleaching and killing coral in waters around the peninsula. Phoenix had ....

Wind turbines play a pivotal role in the global transition to sustainable energy sources. However, the harsh environmental conditions in which wind turbines operate, such as extreme temperatures, high humidity, and exposure to various contaminants, p....

Wind energy remains the leading non-hydro renewable technology, and one of the fastest-growing of all power generation technologies. The key to making wind even more competitive is maximizing energy production and efficiently maintaining the assets. ....

The allure of wind turbines is undeniable. For those fortunate enough to visit these engineering marvels, it’s an experience filled with awe and learning. However, the magnificence of these structures comes with inherent risks, making safety an abs....

Not enough people know that hydrogen fuel cells are a zero-emission energy technology. Even fewer know water vapor's outsized role in electrochemical processes and reactions. Producing electricity through a clean electrochemical process with water....

In the ever-evolving landscape of sustainable transportation, a ground-breaking shift is here: 2024 ushers in a revolutionary change in Electric Vehicle (EV) tax credits in the United States. Under the Inflation Reduction Act (IRA), a transforma....

The fact that EV charging is currently cheaper than filling up your traditional gas tank has set a precedent that public EV charging will always remain less expensive. This is certainly a good thing to support the adoption of EVs, but the high infras....

Now more than ever, it would be difficult to overstate the importance of the renewable energy industry. Indeed, it seems that few other industries depend as heavily on constant and rapid innovation. This industry, however, is somewhat unique in its e....

University of Toronto’s latest student residence welcomes the future of living with spaces that are warmed by laptops and shower water. In September 2023, one of North America’s largest residential passive homes, Harmony Commons, located....

For decades, demand response (DR) has proven a tried-and-true conservation tactic to mitigate energy usage during peak demand hours. Historically, those peak demand hours were relatively predictable, with increases in demand paralleling commuter and ....